Sarah Jamali

Senior Director, Client InsightsComscore

It’s no secret that times are tough out there – it seems that everywhere we look (and go), all we hear (and see) is somehow related to the rising cost of living.

Although inflation seems to be tapering off, the effect of the incredible leaps and bounds observed in prices over the last few of years is still reverberating, with consumers balancing their needs and spending as they face unprecedented cost increases across the board, from automobiles to travel to groceries. Apparel is no exception, and some might argue that the industry has been under extra scrutiny as consumers are cautious and mindful of curbing their discretionary spending in hopes of contributing to their “rainy day” funds and absorbing the increases affecting mandatory, basic necessities such as shelter and food.

That being said, apparel brands, in particular luxury goods, have shown no signs of scaling back their year over year price hikes, perhaps under the assumption that if one can afford such goods during dire economic times, then one can likely afford to pay a premium year after year. That, in conjunction with rising concerns about the environmental impact of fast fashion, as well as an overall categorical rebrand from the less desirable term of “second hand” to “pre-loved” or “consignment”, has contributed to the rise and popularity of resale sites. Namely websites where consumers can post and sell apparel and accessories they no longer want or need to a host of eligible shoppers across the country; adding some extra dollars to sellers’ pockets that can go towards new shopping trips, while buyers can get items “new to them”, as both groups also contribute to reducing the apparel industry’s global carbon footprint.

Taking a look at the most popular resale sites, we see that growth and engagement has increased over the last couple of years, whereas the apparel industry as a whole experienced double-digit declines. More specifically, by looking at the total number of visits made to the most frequented resale sites in May 2024, we observed that visits to these sites collectively grew 3 percent over the last two years while visits to apparel sites declined 30 percent over the same period. It is interesting to note that the increase in resale site visitation mimics trends observed across other industries and other online behaviors, where an increase in mobile visitation has offset declines in desktop visitation.

While some consignment shoppers are perusing and “window shopping” sites to see if something piques their interest, others are purposefully looking for one specific item, and visit all sites in hopes of finding the exact item, color and size of interest. Given its breadth of product offerings, Poshmark is the most cross-visited resale site on both desktop and mobile among shoppers of other competitor sites. On desktop, approximately one quarter of shoppers visiting Depop, Mercari, The RealReal, Vestiaire Collective or ThredUp also visited Poshmark. These rates are even more pronounced on mobile, where more than half of all mobile shoppers visiting Depop, Mercari, The RealReal or ThredUp also visited Poshmark on their mobile devices. With Poshmark emerging as one of the most popular of resale sites, which other resale sites do their shoppers also visit most? The answer is overwhelmingly Mercari, where roughly one third of Poshmark shoppers on either desktop or mobile also browsed Mercari (Source: Comscore Desktop & Mobile Panel; May 2024).

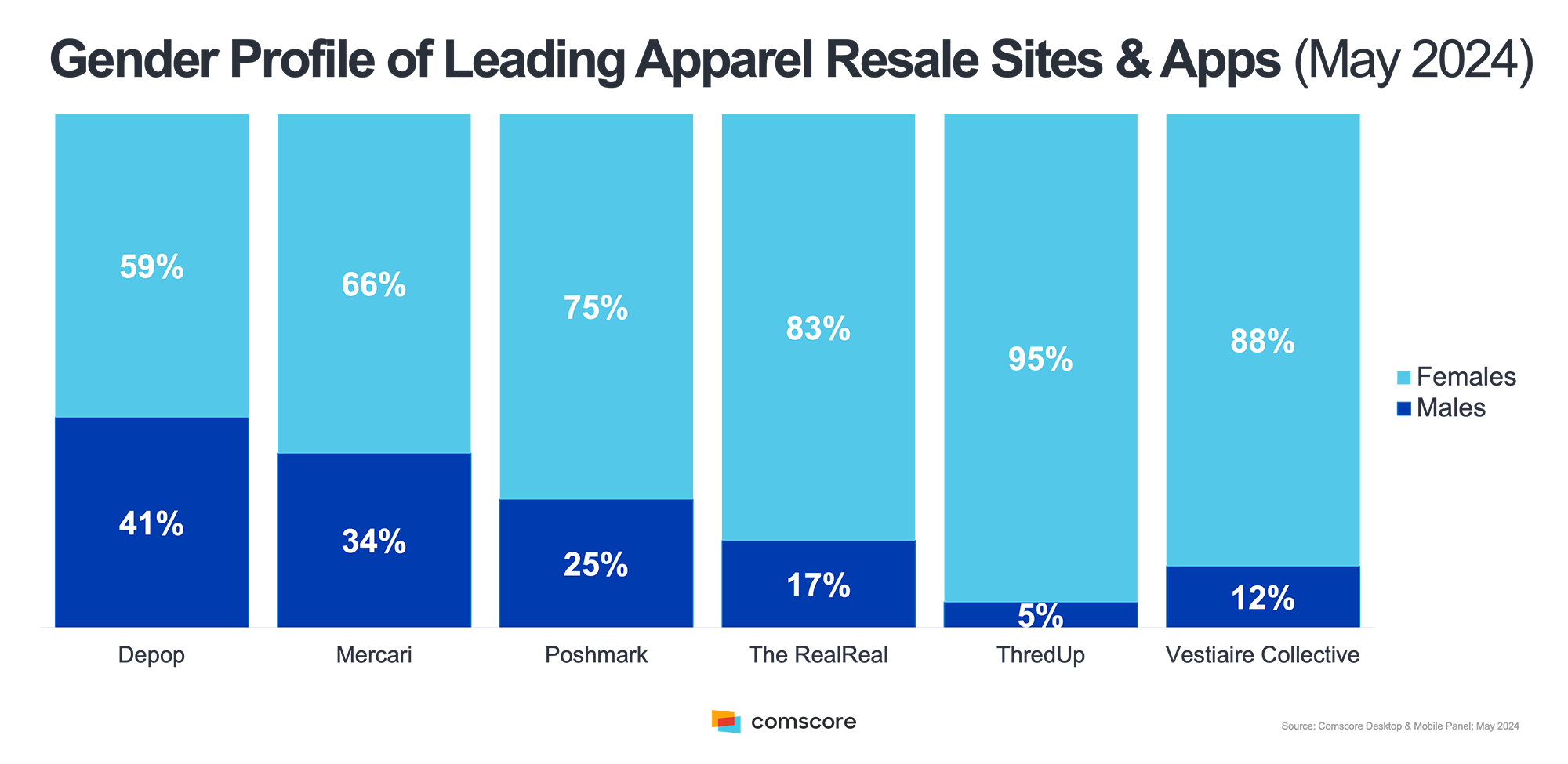

Who are these resale shoppers? It may not be who you think. Digging deeper into each site’s demographic composition, we see that the typical resale shopper skews female, as do most apparel sites (exhibit 1). However, from an income perspective, long gone are the days where the perception around resale shoppers leans towards a less financially developed population – nearly half of today’s shoppers earn a household income of more than $100K a year, an indication of savvy shoppers with an eye for luxury who are willing to spend their hard-earned money on the right item (exhibit 2). Additionally, in terms of age, we see a lot of variety depending on each site’s brand positioning (exhibit 3), where Depop and Vestiare Collective skew towards Gen Z and younger, while more luxury-oriented sites, such as The RealReal and Poshmark, resonate with older shoppers who are at a later stage in life and have had more time to be exposed, and appreciative, of luxury goods.

Exhibit 1

Exhibit 2

Exhibit 3

With the shift towards mobile visitation, social media presence is as critical a tool as ever for brands to reach and engage their target audience who spend a large share of their free time perusing and interacting with brands and their social networks on social media. In May 2024, Instagram was the most successful platform for all brands, eliciting the greatest number of actions and reactions by post relative to all other social platforms, up 20 percent from the previous year (exhibit 4). Not surprisingly, given their demographic profile, those exposed to Depop and Vestiaire Collective content on Instagram were the most reactive, reinforcing the importance for brands to marry their social media strategies with the platforms and usage behaviors most aligned with their target demographic.

Exhibit 4

As inflation eases up, and the economy shows signs of rebounding, it will be interesting to see how, or if, the popularity of resale sites shifts. Urban legend has long speculated that it takes three weeks to form a habit. With evidence of the endless financial and environmental benefits of consignment shopping, and a lessened stigma around the idea of purchasing pre-owned or used items, this “habit” may very well be here to stay and may shift the apparel market as we know it.

Contact us here if you'd like to continue the conversation about emerging trends in the Retail and Apparel space.